Do you dream of quitting that endless grind at work, but bills and debts keep you chained to your desk day after day? Lots of folks feel trapped like that, working decades just to scrape by in retirement, with no time left for fun or family. The FIRE Movement changes all that; it stands for Financial Independence, Retire Early, and get this, some people hit it by age 40 through smart saving and investing.

In this post, we’ll break down simple steps to boost your savings, cut costs, and build wealth that lasts, so you can live life on your terms sooner. This guide packs the tools you need. Stick around to spark your own path.

What Is the FIRE Movement?

Have you ever dreamed of ditching the nine-to-five grind way before your golden years? The FIRE movement, which stands for Financial Independence Retire Early, empowers folks like you to save aggressively, invest smartly, and break free from the paycheck-to-paycheck cycle sooner than you might think.

Definition and Core Principles

FIRE stands for Financial Independence, Retire Early. This movement pushes folks to build enough wealth to quit their jobs way before age 65. Imagine ditching the 9-to-5 grind in your 30s or 40s, living on investments instead.

At its heart, FIRE focuses on extreme savings and smart investing. You slash expenses through frugality, boost your savings rate to 50% or more of income, and let compound growth do the heavy lifting. Budgeting becomes your best friend, turning every dollar into a step toward economic independence.

Core principles keep things simple yet powerful. Prioritize passive income from stocks or real estate. Cut out wasteful spending, like that daily latte habit that adds up fast. Folks chase financial planning that builds long-term wealth, not quick riches.

Think of it as planting seeds today for a lush garden tomorrow. Early retirement isn’t just a dream; it’s a calculated plan with discipline at the core. Savings strategies and investment planning guide every choice, creating a lifestyle design free from money worries. Curious about how FIRE got started? Let’s explore its origins and growth next.

Origins and Growth of the Movement

Now that you understand the definition and core principles of financial independence, let’s trace the roots of this movement back to its start.

People first sparked the FIRE idea in the early 1990s. Vicki Robin and Joe Dominguez wrote “Your Money or Your Life” in 1992. Their book pushed frugality and smart savings to break free from work.

It showed readers how to track expenses, build wealth, and rethink lifestyle choices. Bloggers later fueled the fire. Jacob Lund Fisker launched Early Retirement Extreme in 2007. He shared extreme saving strategies for quick financial freedom.

Then, Pete Adeney, known as Mr. Money Mustache, started his blog in 2011. He used humor and real stories to promote investments, passive income, and early retirement. These voices turned personal finance into a shared adventure.

Trade money for time, not time for money. – Vicki Robin

The movement grew fast in the 2010s. Online forums like Reddit’s r/financialindependence exploded with tips on budgeting techniques and wealth building. Podcasts and books spread the word on frugal living and investment planning.

More folks chased economic independence amid rising costs. They formed meetups and groups to swap ideas on retirement planning and financial literacy. Social media amplified success tales, like quitting jobs in their 30s. This buzz drew diverse crowds, from young professionals to families seeking lifestyle design.

How Does the FIRE Strategy Work?

Ever wondered how folks quit their jobs in their 30s, living off savings like a boss? Imagine you slash expenses, pump up investments, and watch your money grow like wildfire, setting you free sooner than you think.

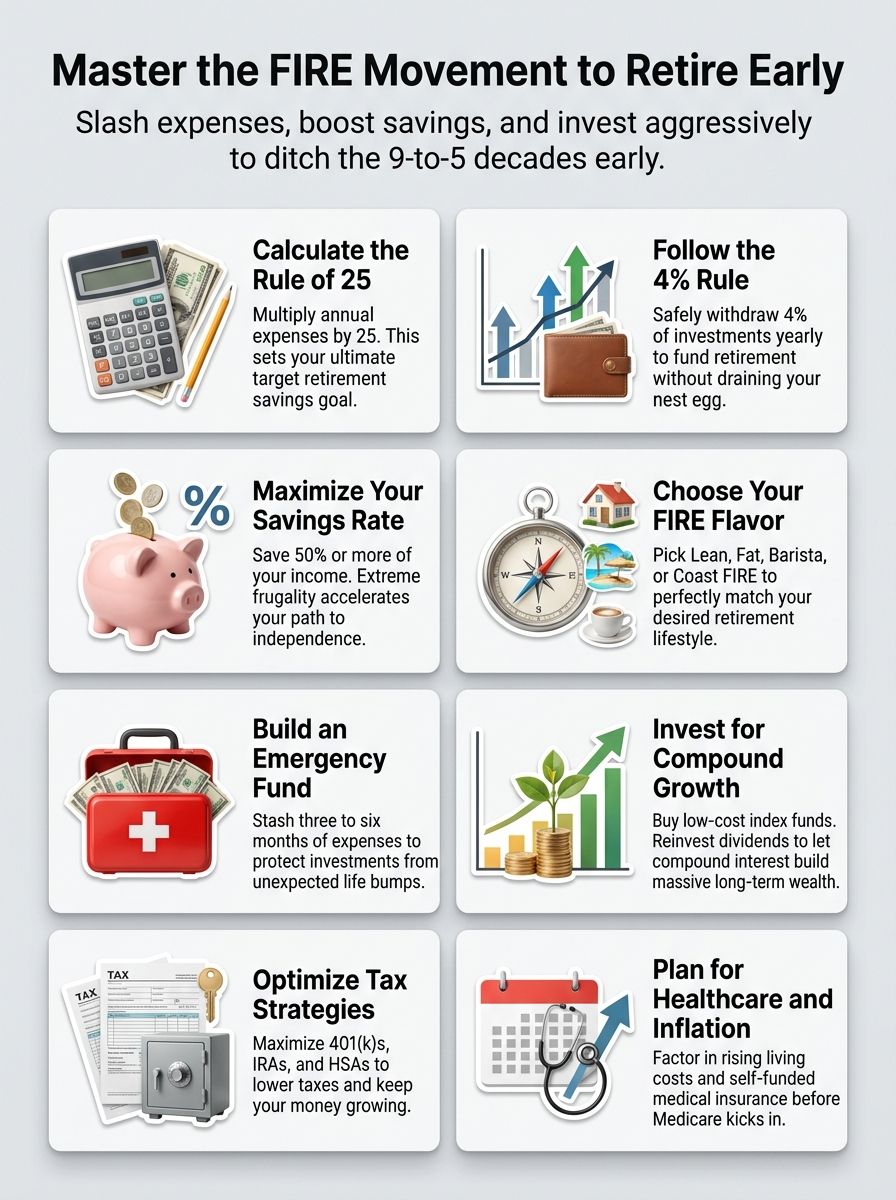

The Rule of 25

The Rule of 25 acts as a simple guide in the FIRE movement. You take your annual expenses and multiply them by 25. This number shows the savings goal for financial independence. Say you spend $40,000 a year, then aim for $1 million in investments. People use this to build wealth through smart saving strategies and frugal living. It relies on compound growth over time.

Folks often pair it with the 4% withdrawal rule for early retirement. Your nest egg generates passive income without running dry. Imagine quitting your job at 40, thanks to careful budgeting and investment planning. This approach boosts economic independence, letting you focus on passions. Just calculate your own figure to see the path ahead.

The 4% Withdrawal Rule

People call the 4% withdrawal rule a key tool in the FIRE movement for early retirement. This rule lets you pull out 4% of your total investments each year to cover living costs. Experts based it on past market data, showing it can make your savings last 30 years or more.

Imagine you save $1 million. You withdraw $40,000 in year one, then adjust for inflation later. Frugality helps here, as it stretches your wealth further.

Investors use this rule to plan passive income without running out of money. Focus on a mix of stocks and bonds for steady growth. High savings rates build that nest egg faster. Picture sipping coffee on a beach, funded by smart financial planning.

This approach reduces stress and boosts economic independence. Savings Rate and Compound Growth. Once you understand the 4% withdrawal rule for safe spending in retirement, focus shifts to growing your wealth upfront. Savings rate drives the FIRE journey. It shows what portion of your income you tuck away.

Aim high, like 50% or more. This speeds up financial independence. Cut costs through frugality. Boost earnings with side gigs. Track every dollar in your budget. High savings fuel investments. They grow your nest egg fast.

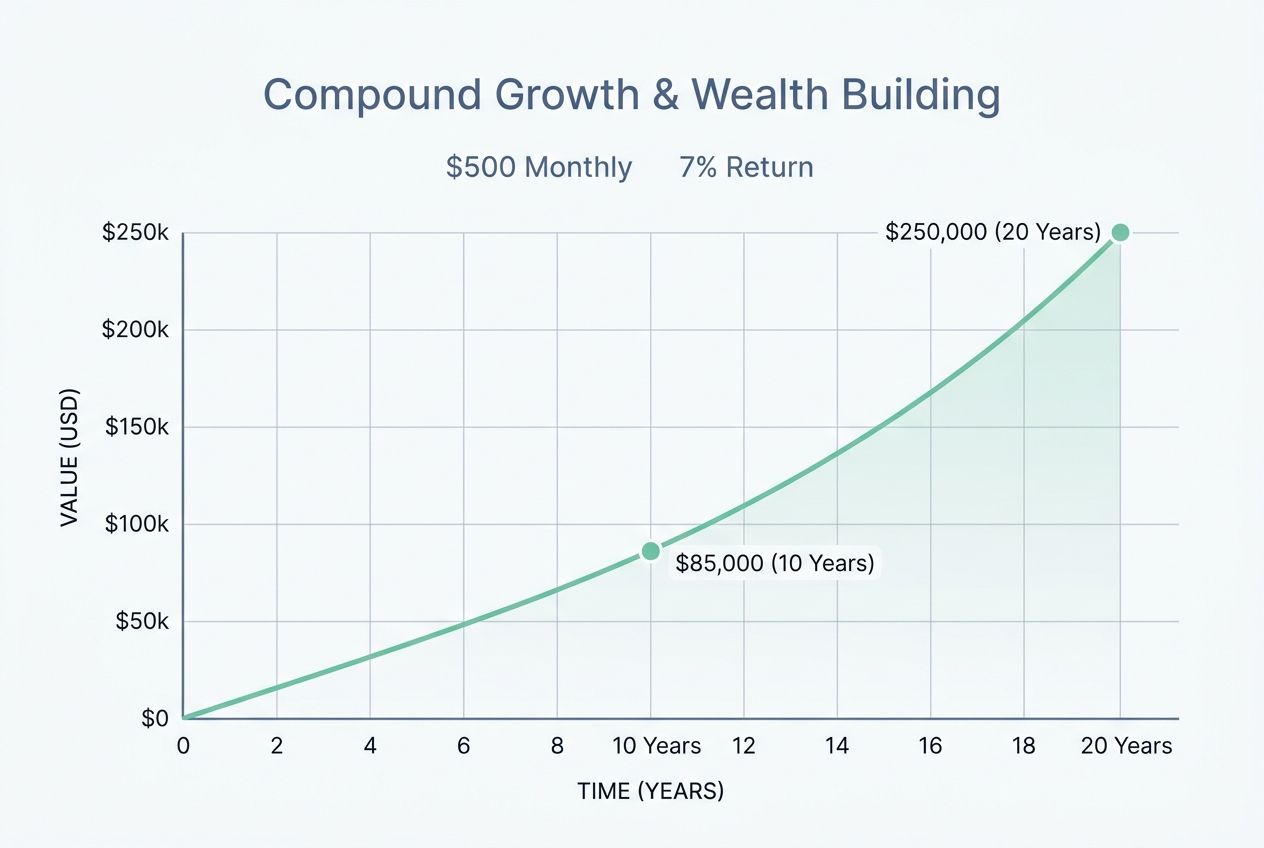

Compound growth works like a snowball rolling downhill. Invest early, and returns build on themselves. Say you save $500 a month at 7% return. In 10 years, it hits over $85,000. Double that time, and it soars past $250,000.

Reinvest dividends for extra power. Choose low-cost index funds for steady gains. Stay patient through market dips. This builds wealth for early retirement. Design a lifestyle that matches your goals. Passive income streams enhance the ride.

Types of FIRE

You know, the FIRE path isn’t one-size-fits-all; it branches into flavors that match your dreams and comfort zone. Picture picking a route that lets you sip coffee while your savings grow, or go all out for luxury—each one sparks that thrill of freedom, so keep reading to find your fit.

Lean FIRE

Lean FIRE focuses on financial independence with a frugal twist. People chase this path by slashing expenses to the bone, building savings through strict budgeting. They aim for a smaller nest egg, often around $500,000 to $1 million, enough for basic needs in early retirement.

Imagine living like a minimalist monk, where every dollar stretches further. Savings rate skyrockets here, thanks to smart frugality and low-cost lifestyle design.

Investments play a key role in Lean FIRE, too. Folks pour money into low-fee index funds for steady wealth building. They target that 4% withdrawal rule on a lean budget, dodging fancy vacations or big homes.

This approach frees up time for passions, but it demands discipline, like skipping daily lattes. Early retirement feels closer when passive income covers the essentials.

Fat FIRE

Fat FIRE suits folks who crave a plush lifestyle in early retirement. You build a big nest egg, often over $2.5 million, to support fancy trips, nice homes, and hobbies without pinching pennies.

People chase this path by ramping up investments and passive income streams. Think of it like planting a money tree that grows fat apples; you pick plenty each year.

Savings rate matters here, but you skip extreme frugality for balanced wealth building. Aim for the 4% withdrawal rule on a hefty portfolio, pulling $100,000 yearly from that $2.5 million stash.

Many hit financial independence in their 40s this way, trading high-paying jobs for freedom. Picture sipping coffee on a beach, your budget lets you splurge on experiences that spark joy.

Barista FIRE

If Fat FIRE feels like aiming for the luxury suite, Barista FIRE offers a cozy middle ground that mixes work with freedom. People chase this path by saving enough to cover basic needs through investments, then taking a low-key job like serving coffee for extra cash and perks.

Imagine stashing away funds until your nest egg hits a safe spot, say following the 4% withdrawal rule for steady income. You keep some frugality in play, but that part-time gig handles health insurance or fun money, easing the push for full retirement.

This style suits folks who want financial independence without ditching all work vibes. Savings rates still matter here, pushing for smart budgeting and passive income streams. Think of it as coasting on your wealth building while sipping lattes on the job, no full stop required. Early retirement gets flexible, letting you focus on passions with less stress from bills.

Coast FIRE

Coast FIRE lets you hit financial independence by saving enough early on, so your investments grow on their own to cover retirement needs. Imagine: you front-load your savings and investments, then ease off the gas pedal.

Work becomes optional, maybe just a side gig for fun or extra cash. People love this path because it blends frugality with smart wealth building, giving you freedom sooner without total burnout.

Say you’ve crunched the numbers and your nest egg will compound to your target through passive income by age 65. Now, coast along with lighter budgeting, focus on passions, and enjoy lifestyle design.

This approach suits those who want economic independence but hate extreme penny-pinching forever. Hey, it beats grinding away until you’re gray!

Key Steps to Achieve Financial Independence

Want to break free from the daily grind and chase financial freedom? Start by tracking every dollar you spend, like a detective on a money trail, and cut out those sneaky expenses that add up fast.

Budgeting and Expense Control

Start budgeting by tracking every dollar you spend. You spot leaks in your wallet fast this way. Cut back on non-essentials, like that daily latte, and watch savings grow. Frugality becomes your best friend in the FIRE movement.

Picture it as training for a marathon; small steps build big wealth over time. Aim for a high savings rate, say 50% of your income, to speed up financial independence.

Control expenses with simple tools, folks. Apps track your spending in real time. They help you stick to a plan without stress. Focus on needs over wants for a frugal living style.

This boosts your passive income potential down the line. Early retirement feels closer when you master budgeting techniques. Your lifestyle design shifts toward economic independence, one smart choice at a time.

Building an Emergency Fund

Once you’ve nailed down your budgeting and expense control, it’s time to build that safety net known as an emergency fund. This fund acts like a financial airbag, cushioning you from life’s unexpected bumps, such as car repairs or sudden job loss.

Experts suggest aiming for three to six months of living expenses tucked away in a high-yield savings account. Think of it as your peace-of-mind buffer, helping you avoid dipping into investments or racking up debt during tough times.

Set small goals to grow this fund fast, like stashing away $1,000 first, then building from there through automatic transfers from your paycheck. High savings rates boost your financial independence journey, letting you focus on wealth building without constant worry.

Folks in the FIRE movement swear by this step, as it frees up mental space for early retirement dreams and a frugal lifestyle. Keep it liquid and easy to access, but resist the urge to touch it for non-emergencies, like that tempting vacation splurge.

Investing Wisely for Long-Term Growth

After you build that emergency fund, it’s time to put your money to work through smart investing, which builds wealth for financial independence. Start with low-cost index funds or ETFs that track the stock market.

These options spread your risk and aim for steady growth over time. Diversify across stocks, bonds, and real estate to weather market ups and downs. Think of it like planting a garden; you water it with regular contributions, and compound interest helps it bloom into a lush retirement nest egg.

Aim for a mix that matches your risk tolerance and timeline to early retirement. Use tax-advantaged accounts like 401(k)s or IRAs to boost your savings rate. Track your investments quarterly, but avoid constant tinkering, as patience pays off in wealth building.

Many in the FIRE movement target 7-10% annual returns through passive income strategies. Stay frugal, reinvest dividends, and watch your financial planning turn into real economic independence.

Tax-Efficient Strategies

Tax-efficient strategies help you keep more money in your pocket for financial independence. Use accounts like 401(k)s and IRAs to lower your taxes on investments. Contribute to a Roth IRA, and your money grows tax-free for retirement.

Max out employer matches in your 401(k); that’s free cash boosting your wealth. Think of it like planting seeds in fertile soil; they sprout faster without weeds of high taxes pulling them down.

Health Savings Accounts offer another smart move for frugal living. Put pre-tax dollars in for medical costs, and invest the rest for passive income later. Avoid early withdrawals to dodge penalties, keeping your savings rate high.

Picture your budget as a leaky bucket; these strategies plug the holes so your early retirement dreams fill up quicker. Stay on top of tax laws; they change, but smart planning turns them into allies for your lifestyle design.

Challenges and Limitations of FIRE

Hey, chasing that FIRE dream can hit some rough spots, like figuring out ways to tap retirement funds without big penalties, dealing with pricey health care that bites into your budget, or watching inflation and stock market dips eat away at your nest egg. Stick around to see smart ways to push past these bumps.

Accessing Tax-Advantaged Accounts Early

People in the FIRE movement often save big in tax-advantaged accounts like 401(k)s and IRAs for financial independence. They face penalties if they pull money out before age 59.5. You pay a 10% fine plus taxes on early withdrawals.

This hurts early retirement plans. Smart folks use strategies to dodge these hits. One way taps the Roth IRA conversion ladder. You shift funds from a traditional IRA to a Roth IRA over time.

Wait five years, and you access that money without penalties. This boosts your savings and investments for long-term wealth building.

Another trick follows Rule 72(t) for substantially equal periodic payments. You take set amounts each year based on life expectancy. This avoids the 10% penalty. Stick to the plan for at least five years or until age 59.5, whichever comes later.

These moves demand careful financial planning and budgeting. They help with frugality and passive income goals. Picture a friend who retired at 40 by mastering these rules; he now enjoys a stress-free lifestyle chasing passions. Talk to a tax pro to make it work for your early retirement dreams.

Healthcare Costs and Coverage

Healthcare costs can hit hard in the FIRE journey, especially if you retire early. You lose employer-sponsored insurance before Medicare kicks in at 65, so plan ahead. Many folks turn to the Affordable Care Act for coverage, but premiums add up fast without subsidies.

Imagine quitting your job at 40, only to face a medical bill that wipes out your savings – talk about a plot twist in your financial independence story. Frugal living helps, yet unexpected health issues demand smart budgeting for these expenses.

High deductibles and out-of-pocket costs test your wealth-building efforts. Shop around for plans that fit your lifestyle design, like high-deductible options paired with HSAs for tax-efficient strategies.

Early retirement freedom feels great, but skimping on coverage risks big setbacks. Let’s look at how inflation and market volatility add more hurdles.

Inflation and Market Volatility

Beyond those healthcare hurdles, inflation and market volatility sneak up as sneaky thieves in your financial independence journey, eroding your savings and shaking up investments.

Inflation creeps in like a slow burn, raising the cost of living year after year, which means your retirement nest egg might not stretch as far as you planned. Think about it, if prices climb by 3% annually, that $1 million portfolio loses real value fast without smart adjustments.

Market volatility adds the wild ride, with stock dips and booms testing your nerves, potentially slashing withdrawal rates during a downturn.

Folks in the FIRE movement counter this by padding their budgets with extra frugality and diverse investment strategies, like mixing stocks with bonds for steadier growth. You build in buffers, say by aiming for a higher savings rate to combat rising costs. Stay vigilant, tweak your financial planning often, and these beasts won’t derail your path to early retirement freedom.

Advantages of the FIRE Movement

Imagine ditching that daily grind years ahead of schedule, freeing up time to chase dreams that light you up. Picture slashing money worries, so you pour energy into hobbies, travel, or family moments that truly count, making life feel like a grand adventure.

Gaining Early Retirement Freedom

Picture a life where you call the shots, not your boss. The FIRE movement hands you early retirement freedom through smart financial independence. You stack up savings and investments to cover your needs without a job.

Folks like Vicki Robin, co-author of “Your Money or Your Life,” sparked this idea back in 1992. By embracing frugality and high savings rates, people retire in their 30s or 40s. Take Pete Adeney, known as Mr.

Money Mustache; he quit work at 30 after aggressive wealth building. This path opens doors to travel, hobbies, or just relaxing. Savings grow with compound interest, turning modest income into lasting security.

Early retirement means ditching the daily grind for what lights you up. You design your lifestyle around passions, not paychecks. Budgeting techniques and investment planning make it real.

Passive income from stocks or rentals keeps cash flowing. One guy saved 70% of his pay and retired at 35; now he bikes across countries. Frugal living cuts costs, boosting economic independence. Retirement planning like this feels empowering, right? It shifts focus from survival to thriving. FIRE slashes financial stress, too, as we’ll see next.

Reducing Financial Stress

FIRE slashes financial stress like a sharp knife through butter. You build wealth with smart savings and investments. This creates a safety net for tough times. No more lying awake at night over bills. Frugality becomes your ally, turning small habits into big wins for financial independence.

Picture early retirement without the money worries; it frees your mind for passions. Budgeting keeps expenses in check, boosting passive income streams. Readers often share stories of ditching debt, feeling lighter than air. Wealth building through these steps eases the load, letting you design a calmer lifestyle.

Enhancing Focus on Passions and Experiences

Imagine ditching the daily grind that steals your time. Financial independence lets you chase passions, like painting landscapes or hiking trails you’ve always dreamed about. You build wealth through smart investments and frugal living.

This shift frees up hours for experiences that matter. Think family adventures or learning guitar. Early retirement opens doors to a richer lifestyle.

People in the FIRE movement often share stories of joy from this focus. One reader quit their job to travel Europe on passive income. Savings strategies and budgeting make it possible.

You reduce stress and embrace what lights you up. Wealth building supports these choices. Frugality turns into freedom for hobbies and memories.

Wrapping Up

You chase financial independence through the FIRE movement, and it sparks real change in your life. Picture saving big on daily costs, like skipping that fancy coffee run to boost your investments.

Folks in this community build wealth with smart budgeting and frugal living. They aim for early retirement, free from the nine-to-five grind. Passive income streams keep the lifestyle flowing smoothly. You can join them, turning small steps into big wins.

Grab hold of these ideas and tweak them for your path. Frugality pairs well with wise investment planning, growing your nest egg fast. Economic independence means more time for passions, less worry about bills.

Folks share stories of quitting jobs early and traveling the world on a budget. Your savings rate matters; crank it up to speed toward retirement planning goals. Start today, watch your financial literacy soar, and enjoy the ride to a richer life.

FAQs on the FIRE Movement

1. What is the FIRE Movement, anyway?

FIRE stands for Financial Independence, Retire Early, and it’s all about saving big bucks so you can quit the daily grind sooner than most folks dream. Picture this: you’re sipping coffee on a beach while your investments work for you, no boss in sight. It’s like hitting the jackpot without buying a ticket, but it takes smart planning and a bit of grit.

2. How can I achieve financial independence faster with FIRE?

Boost your savings rate to 50% or more of your income, and invest in low-cost index funds to grow your nest egg. Cut back on those impulse buys, like that fancy latte habit, and watch your money multiply.

3. What role does frugality play in the FIRE Movement?

Frugality is the secret sauce that speeds up your path to financial freedom; it means living below your means, dodging debt, and focusing on what truly matters. Think of it as training for a marathon, where every penny saved gets you closer to the finish line without burning out.

4. Are there risks in chasing FIRE too quickly?

Yes, rushing can lead to burnout or skimping on health insurance, so balance is key. Always keep an emergency fund handy, because life throws curveballs, and you don’t want to strike out.