Have you jumped into cryptocurrency investments, only to feel lost when tax season rolls around? Many folks buy Bitcoin or Ethereum, excited about quick gains, but then panic hits. They worry about surprise tax bills from the IRS. It’s like finding a hidden fee in your favorite game, right? You thought you won big, but Uncle Sam wants his share.

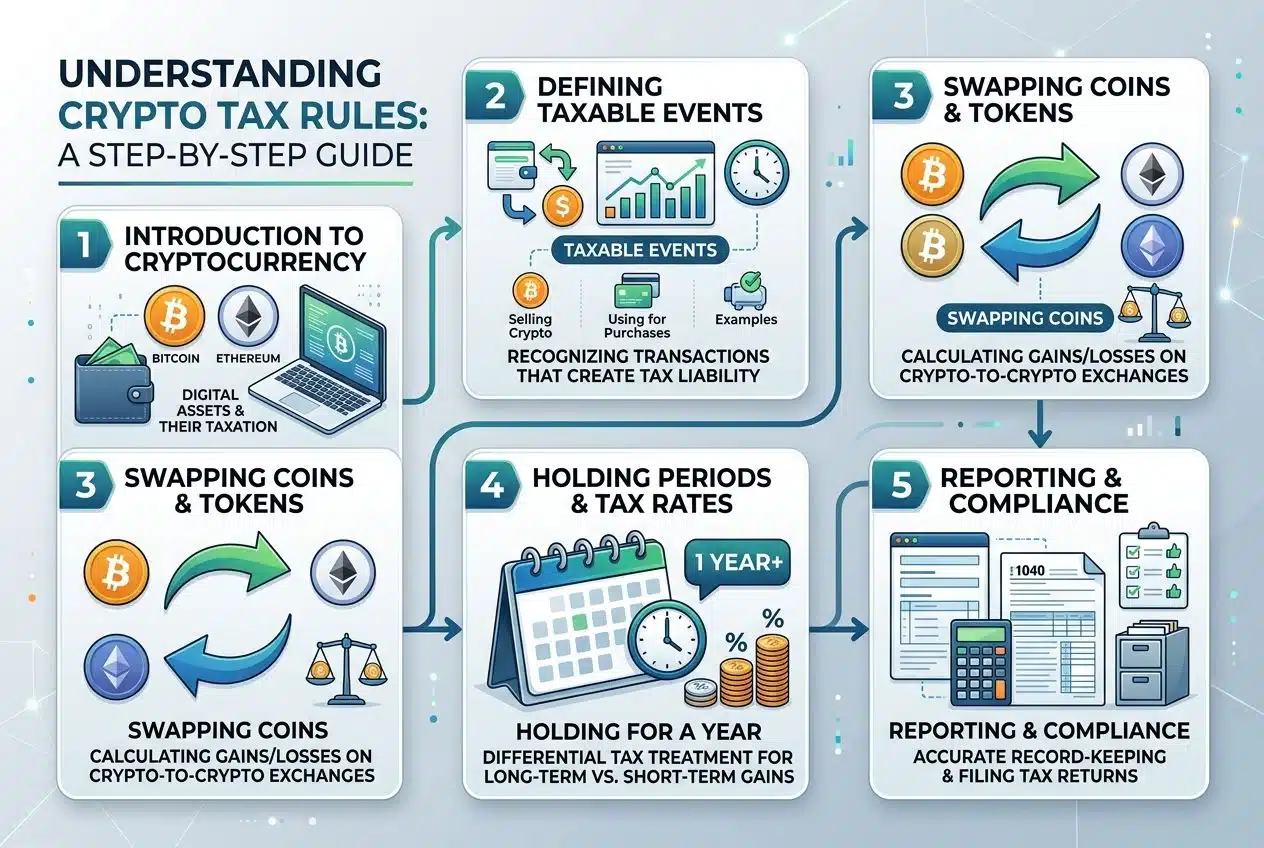

The IRS treats cryptocurrency as property, not cash, so you pay taxes on profits from sales or trades. That’s a key fact to grasp in Crypto Tax Rules. This blog post breaks it down step by step, with tips to track your trades and cut your tax hit.

You’ll learn taxable events, like swapping coins, and smart moves, such as holding for a year to lower rates. Stick around for the full scoop.

Understanding Cryptocurrency and Taxes

Cryptocurrency acts like digital cash, secured by blockchain, letting folks trade without banks, kind of like swapping baseball cards in a high-tech playground. The IRS sees it as property, not currency, which means your trades could trigger taxes, so keep reading to dodge those surprises.

What is cryptocurrency?

Cryptocurrency represents a paradigm shift in how we think about money and value exchange. – Anonymous Blockchain Expert

People create cryptocurrency as a form of digital money. They secure it with codes, not banks. You store it in online wallets, like a virtual safe. Bitcoin started it all in 2009, sparking a wave of digital assets. Investors trade these on exchanges, aiming for gains.

Folks use cryptocurrency for payments or holdings. It runs on blockchain, a shared ledger that tracks every move. This setup cuts out middlemen, making deals fast and cheap. Think of it as email for money, zipping value around the globe. Tax rules treat it like property, hitting you with capital gains on sales.

How does the IRS classify cryptocurrency?

Now that we’ve covered the basics of what cryptocurrency is, let’s shift gears to how the IRS sees it in the tax world. The IRS classifies cryptocurrency as property, just like stocks or real estate.

They issued Notice 2014-21 back in 2014 to make this clear. This means general tax rules for property apply to your digital assets. You face capital gains taxes when you sell or trade them. Think of it as owning a piece of art; if you sell it for more than you paid, you owe taxes on the profit.

Folks often mix this up with actual money, but the IRS says no, it’s not currency for tax purposes. They treat it under IRS guidelines as virtual currency, a type of digital asset.

This setup affects your tax implications on cryptocurrency transactions. For example, if you mine Bitcoin, that counts as income, not just a hobby reward. Picture your crypto wallet like a stock portfolio; every move could trigger taxable events. Keep good records to stay on top of financial compliance and avoid surprises come tax time.

Taxable Events in Cryptocurrency Investments

Hey, imagine turning your Bitcoin into bucks or swapping it for Ethereum, and bam, Uncle Sam wants a cut. Those everyday crypto moves, like mining rewards or buying coffee with coins, often spark tax bills that catch folks off guard, so keep reading to spot them early and stay ahead.

Selling cryptocurrency for cash

You sell cryptocurrency for cash, and bam, it counts as a taxable event. The IRS sees crypto as property, not currency. Calculate your gain or loss by subtracting what you paid from the sale price.

Short-term capital gains apply if you held it under a year; those match your regular income tax rates. Long-term rates kick in after a year, often lower, like 0% to 20% based on income.

Imagine: You bought Bitcoin at $10,000, sold at $50,000 after six months. Ouch, that $40,000 profit faces short-term capital gains tax. Track every transaction for accurate tax reporting. Use tools to log buys, sells, and values. This keeps you compliant with IRS guidelines on digital assets.

Virtual currency is treated as property for U.S. federal tax purposes. – IRS Notice 2014-21

Trading one cryptocurrency for another

Selling crypto for cash creates a taxable event, and so does swapping one digital asset for another. Imagine you trade Bitcoin for Ethereum, the IRS treats it like you sold the Bitcoin first.

They base the tax on the fair market value at that moment. Capital gains kick in if the value has risen since you bought it. Short-term gains apply if you held it under a year, hitting ordinary income tax rates.

Long-term capital gains offer lower rates for holdings over a year. Keep track of every cryptocurrency transaction for accurate tax reporting. Say you swap tokens on a blockchain platform, it counts as income if you gain value. Losses can offset other gains, easing your tax liabilities.

Use tools to log details like dates and values. This way, you stay on top of IRS guidelines without headaches.

Using cryptocurrency to purchase goods or services

You spend cryptocurrency on a cup of coffee or a new gadget. This counts as a taxable event. The IRS sees it as selling your digital assets for their fair market value at that moment.

Calculate your capital gains or losses. Subtract your cost basis from the value when you make the purchase. Report any profit as capital gains tax on your tax return.

Imagine: you buy a pizza with Bitcoin that has risen in value since you got it. Uncle Sam wants his share. Track the transaction details carefully. Note the date, amount, and market price.

This helps with accurate tax reporting. Short-term gains face higher rates if you held the crypto for under a year. Long-term capital gains apply to holdings over a year, often at lower rates. Stay on top of these cryptocurrency transactions to avoid surprises during tax season.

Earning cryptocurrency through mining or staking

Spending crypto on everyday buys triggers taxes, but what about when you earn more coins? Earning cryptocurrency through mining or staking counts as income tax right away. Imagine you set up a rig to mine Bitcoin, and boom, the IRS sees those new coins as taxable income at their fair market value on the day you get them.

Staking works much the same way; lock up your Ethereum, earn rewards, and yep, those become part of your income tax bill. Folks often forget this hits as ordinary income, not just capital gains later on.

Keep solid records of these cryptocurrency transactions to avoid headaches with reporting requirements. Miners, think of it like running a side hustle; the IRS treats your setup costs as deductions, but you report the full value of earned digital assets.

Stakers face similar rules, with rewards taxed upon receipt, even if you hold them long-term. This ties into the wider tax implications of cryptocurrency investments, so track every detail for smooth tax returns.

Receiving cryptocurrency as payment

Beyond earning crypto through mining or staking, you might get it as payment for your work or services, and that counts as a taxable event too. Imagine: a freelancer accepts Bitcoin for a job.

The IRS sees that as regular income. You report the fair market value in dollars on the day you receive it. This falls under income tax rules for cryptocurrency transactions.

Ignore the date you got paid if the value changes later; lock in that initial amount for tax reporting. Freelancers, watch out, it adds to your total earnings and could bump you into a higher tax bracket.

Keep good records of these digital asset deals to stay on top of IRS guidelines. Hey, it’s like getting cash, but with a blockchain twist that demands sharp financial compliance.

Special Scenarios in Cryptocurrency Taxation

Ever mined crypto and wondered if that counts as income, like finding gold in your backyard? Dig into staking rewards or gifting crypto next, you might save a bundle on taxes with the right moves.

Cryptocurrency mining income

Miners earn cryptocurrency by solving complex puzzles with powerful computers, and the IRS sees this as income right away. You report the fair market value of those coins on the day you mine them as ordinary income.

Picture it like digging up gold; that fresh nugget counts as pay before you even sell it. This hits you with income tax, plus self-employment tax if mining is your gig. Folks often forget that the costs for electricity and gear cut your taxable amount, so track every bill like a hawk.

Staking might seem similar, but mining stands out with its energy demands and hardware needs. Rewards from mining qualify as taxable events under IRS guidelines for digital assets.

Say you mine Bitcoin worth $5,000 in a month; add that to your tax return on Schedule C for business income. Smart investors offset this with deductions, turning a potential tax headache into a manageable part of their investment strategy. Keep detailed records of cryptocurrency transactions to avoid audits, and consult a pro if numbers pile up fast.

Staking rewards and airdrops

Staking rewards come as income when you lock up your crypto to support a blockchain network. The IRS sees these rewards as taxable at their fair market value on the day you get them.

Think of it like earning interest on a savings account, but with digital assets involved. You report this on your tax return as ordinary income. Airdrops happen when projects drop free tokens into your wallet, often for promotion. These count as income too, based on their value when you gain control.

Folks often overlook tracking these events, leading to surprises at tax time. Keep good records of dates and values to stay on top of tax implications. Gifting or donating cryptocurrency brings its own rules, so let’s look at that next.

Gifting or donating cryptocurrency

Gifting cryptocurrency counts as a taxable event under IRS guidelines. You avoid capital gains tax if the gift stays below the annual exclusion limit, which is $17,000 per person.

The recipient takes on your original cost basis for future tax reporting on any sales. Imagine: you hand over Bitcoin to a family member, and it feels like passing a hot potato, but done right, it skips immediate tax hits for you.

Donating digital assets to a qualified charity offers sweet tax breaks. Claim a deduction based on the fair market value at donation time, especially if you held the crypto for over a year to dodge capital gains.

Charities like the Red Cross accept these gifts now, turning your investment strategy into real-world good without extra tax liabilities. Keep records of the transaction date and value for smooth financial compliance on your tax returns.

Types of Taxes on Cryptocurrency

You know, when crypto profits hit your wallet, Uncle Sam wants his share through capital gains tax, which kicks in on those investment sales. Then there’s income tax, treating your earned coins from mining or staking like regular pay, so keep an eye on that to avoid surprises come tax time.

Capital gains tax on crypto investments

Crypto hits your wallet as property in the eyes of the IRS, folks. Sell it for a profit, and capital gains tax kicks in. This tax applies to the difference between what you paid and what you got back.

Picture buying Bitcoin at $10,000, then cashing out at $50,000; that $40,000 gain faces taxation. Short-term gains, from assets held under a year, get taxed like regular income, up to 37 percent based on your bracket.

Ouch, right? Long-term capital gains, for holdings over a year, enjoy lower rates: zero, 15, or 20 percent, depending on your total earnings. High earners might also face the Net Investment Income Tax at 3.8 percent on top.

Track every cryptocurrency transaction to stay on top of tax implications. Use software or spreadsheets for records; the IRS demands details on cost basis and sale prices. Offset gains with losses from other digital assets to cut your bill.

Imagine harvesting losses by selling underwater crypto, then buying back later. This strategy helps with financial compliance under IRS guidelines. Gifting crypto avoids immediate taxes, but watch the $17,000 annual exclusion limit per person.

Donating to charity deducts the fair market value, skipping capital gains altogether.

Income tax on earned cryptocurrency

You earn cryptocurrency through mining, staking, or as payment for work, and the IRS sees this as ordinary income. Report it on your tax return just like regular wages. The fair market value at the time you receive it counts as your income.

Say you mine Bitcoin worth $5,000; you owe income tax on that amount right away. Tax rates depend on your total earnings, often falling between 10% and 37%. Keep good records of these cryptocurrency transactions to avoid headaches later.

Folks sometimes forget about staking rewards or airdrops, treating them like freebies. Nope, those count as income too, hitting your tax liabilities. Imagine getting a surprise airdrop valued at $1,000; Uncle Sam wants his share based on that value.

Use Form 1040 to report this, and consider consulting a tax pro for tricky spots in cryptocurrency taxation. This keeps your financial compliance smooth and stress-free.

Tax Rates for Cryptocurrency Investments

Crypto gains face different tax hits based on how long you hold them, folks. Dig into short-term rates that match your income bracket, or go long-term for sweeter deals that could slash your bill in half, and keep reading to see how it all shakes out for your wallet.

Short-term capital gains tax rates

You know those quick flips in crypto that feel like a win, but then taxes hit? Short-term capital gains apply to assets held for one year or less, and the IRS taxes them at your ordinary income rate.

| Taxable Income Bracket | Short-Term Capital Gains Tax Rate |

|---|---|

| $0 to $11,000 | 10% |

| $11,001 to $44,725 | 12% |

| $44,726 to $95,375 | 22% |

| $95,376 to $182,100 | 24% |

| $182,101 to $231,250 | 32% |

| $231,251 to $578,125 | 35% |

| $578,126 or more | 37% |

Rates match your federal income tax bracket, folks. Sell that Bitcoin after just six months? Uncle Sam takes a cut based on your total earnings. Imagine trading Ethereum for a quick profit, only to owe 24% if you fall in that middle bracket. Brackets adjust yearly, so check IRS updates. Married couples filing jointly see different thresholds, like up to $89,450 for the 12% rate. Keep solid records to avoid surprises.

Long-term capital gains tax rates

Long-term capital gains apply when you hold crypto for over a year before selling, and rates depend on your income bracket.

| Filing Status | 0% Rate Income Threshold | 15% Rate Income Threshold | 20% Rate Income Threshold |

|---|---|---|---|

| Single | Up to $44,625 | $44,626 to $492,300 | Over $492,300 |

| Married Filing Jointly | Up to $89,250 | $89,251 to $553,850 | Over $553,850 |

| Head of Household | Up to $59,750 | $59,751 to $523,050 | Over $523,050 |

These rates, folks, can save you big bucks compared to short-term ones, like dodging a hefty bill at tax time. Picture your Bitcoin sitting pretty for 366 days; it qualifies. High earners, watch out for that extra 3.8% net investment income tax if your modified adjusted gross income tops $200,000 single or $250,000 joint. Rates adjust yearly with inflation, so check IRS updates for 2026. Crypto counts as property here, just like stocks. Now, let’s talk ways to cut that tax hit.

Strategies to Minimize Cryptocurrency Tax Liability

Hey, nobody likes handing over extra cash to Uncle Sam, right? Check out these clever moves to slash your crypto taxes and keep more coins in your pocket.

Holding crypto for the long term

Hold crypto assets for over a year, and you qualify for long-term capital gains tax rates. These rates often sit lower than short-term ones, which match your regular income tax bracket.

Imagine: you buy Bitcoin today, hang onto it through market ups and downs, like a patient gardener waiting for seeds to bloom. Sell after that year mark, and you might pay just 0% to 20% on profits, depending on your income.

This strategy cuts your tax liabilities big time, turning potential headaches into smoother sails. Smart investors eye this approach to boost investment returns while dodging higher taxes on quick flips. IRS guidelines make it clear: time your sales right to tap into those favorable long-term gains.

You feel the relief when tax season rolls around, no massive bill looming. Now, let’s talk about offsetting gains with losses.

Offsetting gains with losses

You sell some crypto at a loss, and that can wipe out gains from other sales. This trick cuts your capital gains tax bill. Imagine your Bitcoin shot up, but your Ethereum tanked – pair them up on your tax return.

The IRS lets you offset short-term gains with short-term losses first. Long-term ones work the same way. Do this right, and you might drop your tax rate on those investment returns.

Extra losses? Carry them forward to future years, easing tax liabilities down the road. Track every cryptocurrency transaction, folks, because sloppy records lead to headaches with IRS guidelines.

One reader shared how he offset a big win with a forgotten altcoin flop – saved him thousands. Stay sharp on these taxation strategies, and your digital assets won’t bite back at tax time.

Utilizing tax-advantaged accounts

Beyond offsetting gains with losses, another smart investment strategy taps into tax-advantaged accounts to cut your tax liabilities on cryptocurrency investments. Think of these accounts as shields that protect your digital assets from immediate capital gains tax hits.

You can use a self-directed IRA, for example, to hold cryptocurrencies like Bitcoin. Trades inside the account stay tax-free until you withdraw funds. This setup lets your investment returns grow without the drag of yearly tax reporting. A Roth IRA offers even sweeter perks, with qualified withdrawals coming out tax-free after age 59½.

Crypto folks often overlook how these accounts fit into broader taxation strategies under IRS guidelines. Pair them with long-term capital gains planning for real power. Say you stash Ethereum in a traditional IRA; you defer income tax on staking rewards until retirement.

This move aligns with financial compliance and boosts your net investment income over time. Just check the rules, as not every platform allows blockchain assets in these setups. It feels like finding a hidden gem in the tax code, right? Keep good records of all cryptocurrency transactions to stay on top.

Reporting Cryptocurrency on Your Tax Return

Reporting Cryptocurrency on Your Tax Return: Imagine you’re sitting down with your coffee, ready to tackle tax season, and you pull out Form 1040 along with any 1099-B forms from your exchanges, while double-checking those detailed records of every crypto buy, sell, or trade to avoid any surprises from the IRS. Craving deeper insights on dodging common pitfalls? Explore the next sections!

Required tax forms (e.g., Form 1040, 1099-B)

You handle cryptocurrency taxes by reporting them on specific forms. These forms help you stay compliant with IRS guidelines on digital assets.

- Form 1040 asks about virtual currency right on the front page, so you check yes if you had any cryptocurrency transactions like selling or trading during the tax year, which ties into your complete tax return and flags the IRS to look for more details on capital gains or income tax.

- Schedule 1 comes into play for extra income from sources like staking rewards or mining, where you report that as ordinary income tax before it flows back to your main Form 1040, keeping everything organized for financial compliance.

- Form 8949 lets you list out each cryptocurrency transaction in detail, such as the date you bought and sold digital assets, the cost basis, and the gain or loss, which is key for accurate tax reporting on investment returns.

- Schedule D summarizes those gains and losses from Form 8949, helping you calculate short-term or long-term capital gains tax rates on your crypto investments, and it attaches right to your tax return for a clear picture of tax liabilities.

- Form 1099-B arrives from exchanges like Coinbase if you traded over certain amounts, showing proceeds from cryptocurrency transactions that you must match up with your own records to avoid misreporting and potential audits under IRS guidelines.

- Form 1099-MISC covers income from things like airdrops or payments in crypto, treating them as taxable events that count toward your income tax, so you include this when filing to handle taxation strategies properly.

- Schedule C fits if you run a crypto mining operation as a business, where you report profits and deduct expenses related to blockchain assets, ensuring you address tax implications on earned cryptocurrency.

Keeping records of crypto transactions

Keeping good records of your crypto transactions saves you from tax headaches down the road. You need them to calculate capital gains and meet reporting requirements accurately.

- Track every cryptocurrency transaction right away, like buys, sells, or trades, to spot taxable events without missing a beat. Note the date, amount in coins, and fair market value in dollars at that moment, because the IRS sees digital assets as property for tax purposes. This habit turns a messy pile of blockchain data into clear proof for your tax returns.

- Use simple tools, such as spreadsheets or crypto tracking apps, to log details on income tax from staking rewards or mining. Include wallet addresses and exchange confirmations, so you avoid underreporting cryptocurrency transactions that could trigger audits. Picture it as your financial diary, keeping everything tidy for long-term gains calculations.

- Record the cost basis for each digital asset you hold, which means jotting down what you paid originally plus any fees. This step helps offset capital gains with losses on your tax forms, and hey, it feels like finding money in an old coat pocket when deductions kick in. Stay consistent, even for small trades, to comply with IRS guidelines on investment returns.

- Save receipts for any cryptocurrency used in purchases or as payment, treating them like income if you earned them through work. Document the fair market value on the day of receipt to figure tax liabilities properly, avoiding surprises during filing season. It’s like building a safety net for your investment strategy in the wild world of digital currency regulations.

- Keep records for at least three years, or longer if the IRS asks, covering everything from airdrops to gifting crypto. Include notes on lost or stolen assets for potential deductions, ensuring financial compliance without the stress. Think of it as your secret weapon against common mistakes in tax reporting for blockchain assets.

Common Challenges and Mistakes in Crypto Taxation

Crypto taxes throw curveballs at folks, like when you mess up reporting transactions or skip some altogether, and figuring out what to do with lost or stolen coins feels like hunting for buried treasure without a map, so dig into the rest of this post to steer clear of these slip-ups.

Misreporting or underreporting transactions

Many folks trip up on tax reporting for cryptocurrency transactions, and it stings when the IRS catches on. You might forget a trade or lowball your capital gains, thinking it’s no big deal, like sweeping crumbs under the rug.

But hey, that can lead to hefty fines or audits, turning your investment strategy into a headache. The tax implications hit hard if you underreport income tax from stakeholder rewards or ignore taxable events altogether.

Keep detailed records of every buy, sell, or swap to stay on the straight and narrow.

Folks often mix up short-term gains with long-term capital gains, messing up their tax returns big time. Imagine telling a fib on your Form 1040; it’s like poking a bear. Digital assets demand spot-on financial compliance under IRS guidelines, so double-check those numbers to dodge penalties. Now, let’s talk about addressing lost or stolen cryptocurrency.

Addressing lost or stolen cryptocurrency

Losing your cryptocurrency to theft feels like a gut punch, doesn’t it? Imagine you wake up one day and, poof, your digital assets vanish from a hacked wallet. The IRS sees this as a potential capital loss, which you can report to offset other capital gains on your tax return.

File it under Form 8949, listing the date of the theft and your cost basis. That move might lower your tax liabilities, turning a bad situation into something less painful.

Stolen crypto demands quick action for tax reporting. Grab evidence like police reports or exchange notifications to back up your claim. The tax implications hinge on proving the loss, so track every detail of those cryptocurrency transactions.

This step helps with financial compliance and avoids IRS headaches down the road. Think of it as patching a leaky boat before it sinks your investment strategy.

The Bottom Line

Crypto taxes boil down to treating digital assets like property, folks. You face capital gains when you sell or trade them for profit. Hold onto your coins for over a year, and you might snag lower long-term capital gains tax rates.

Short-term gains? They hit you with regular income tax rates, which can sting. Track every cryptocurrency transaction to meet reporting requirements on your tax returns.

Think of it as a game where a smart investment strategy cuts your tax liabilities. Offset those gains with losses from other deals. Donate crypto to charity, and you dodge some taxes while doing good.

Stay on top of IRS guidelines for financial compliance, or risk audits. Your blockchain assets deserve that attention for solid investment returns.

FAQs on Crypto Tax Rules

1. Hey, what taxes hit my cryptocurrency investments?

You pay capital gains tax on profits from selling crypto, like Bitcoin or Ethereum. It’s like selling stocks, you know? Report it to the IRS to stay on the right side.

2. How does the IRS view my crypto trades?

The IRS treats cryptocurrency as property, so every trade or sale triggers tax implications. Lost money? You might deduct those losses, turning a sour lemon into lemonade.

3. Do I have to report all my cryptocurrency transactions?

Yes, report them on your tax return if you bought, sold, or traded. Even small ones count. Keep good records to avoid headaches later.

4. What if I mine cryptocurrency? Is that taxable?

Mining counts as income, taxed at your regular rate. Think of it as earning wages from a digital gold rush. Track your costs to offset some taxes.